Why 2026 Is the Year of Mobile-Banking Obsession

March 4, 2026 | 3 min read

In 2026, banks that are not obsessed with their mobile strategy will fall behind.

July 21, 2020|0 min read

Copied

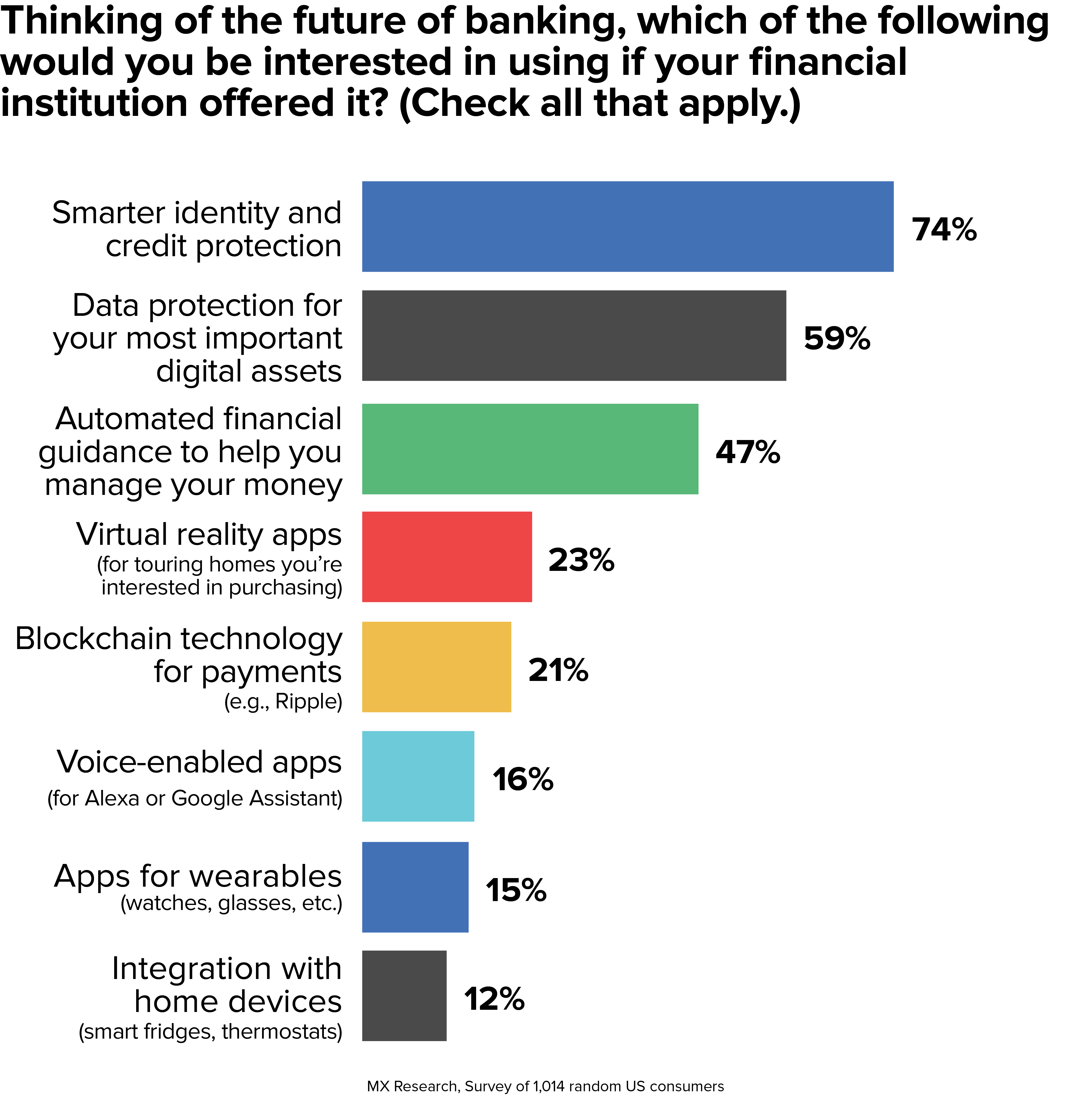

As COVID-19 continues to change the banking industry, it can be hard to know what the future holds. To help make sense of banking today, we surveyed more than 1,000 random U.S. consumers and asked them to list which of eight features they would be most interested in.

Identity and data protection topped the list, as people continue to worry about fraud. Beyond that, people said — at a rate of twice the fourth most-selected option — that they were interested in automated financial guidance to help them manage their money.

In this post, we explore these top three most desired features, looking at how banks can make the most of the future.

Data breaches are increasingly common, and consumers are right to worry. According to findings from Javelin Strategy & Research, there were nearly 17 million victims of identity fraud in 2017 — a record high. And according to Arkose Labs, the third quarter of 2019 saw a 30% increase in overall fraud, with a 70% increase in “bot-driven account registration fraud.”

Fortunately, 64% of consumers say they either completely trust or somewhat trust their financial institutions with their data, while only 15% say they either somewhat distrust or completely distrust them.

And yet, there’s always room for improvement. Offering heightened identity and credit protection can help move consumers closer to completely trusting financial service companies.

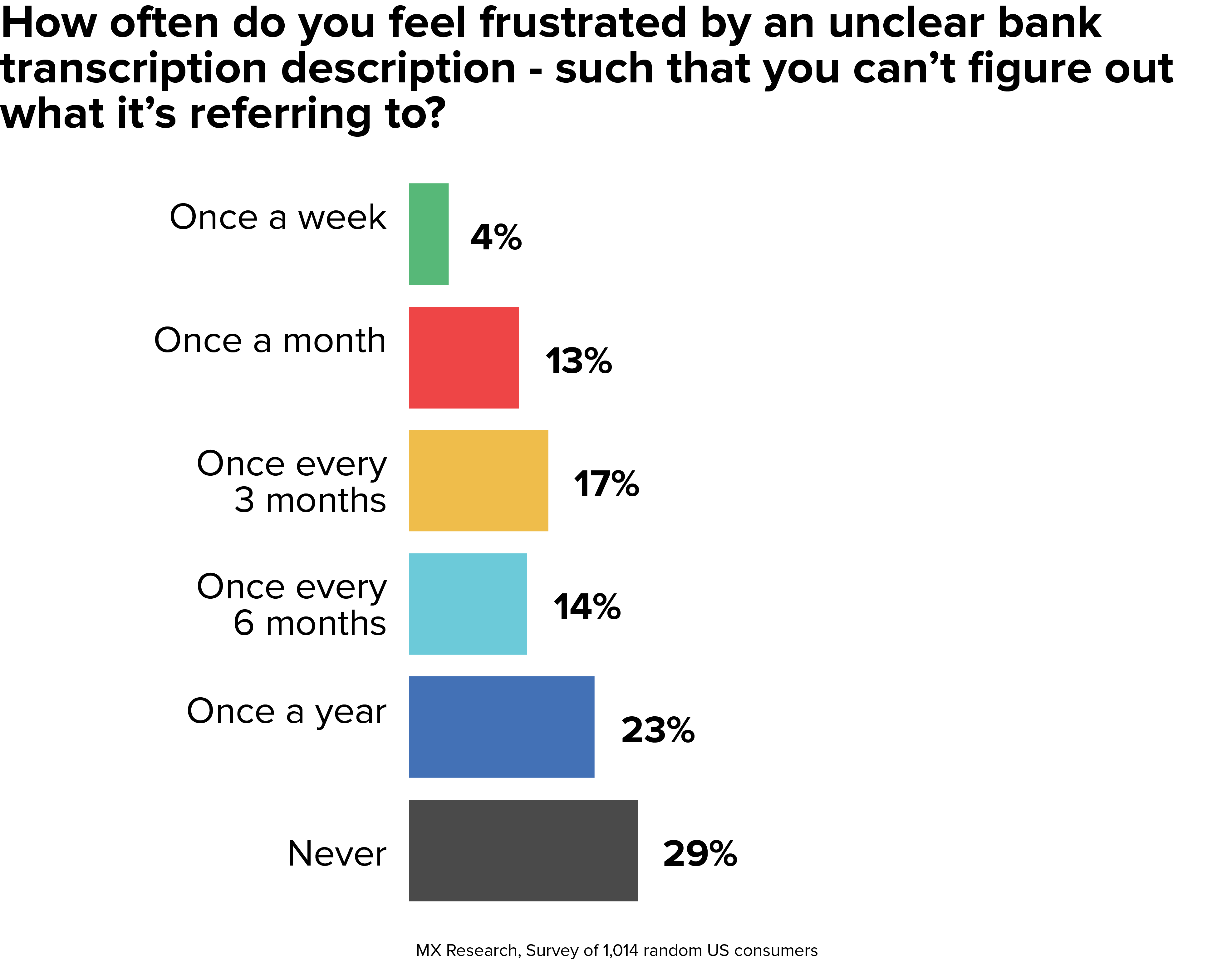

One way to do this is to start with clean data. After all, if your customers can’t understand their transactions — if they have to wade through a string of unclear transaction descriptions — they’ll feel frustrated. It’s an experience 70% of consumers have had.

But this experience of confusion or perceived fraud doesn’t just hurt consumers. It also hurts financial institutions. After all, when people worry about a transaction, they contact the call center, needlessly using up your resources. Offering smart identity and credit protection — rooted in clean data — is an effective way to avoid these issues.

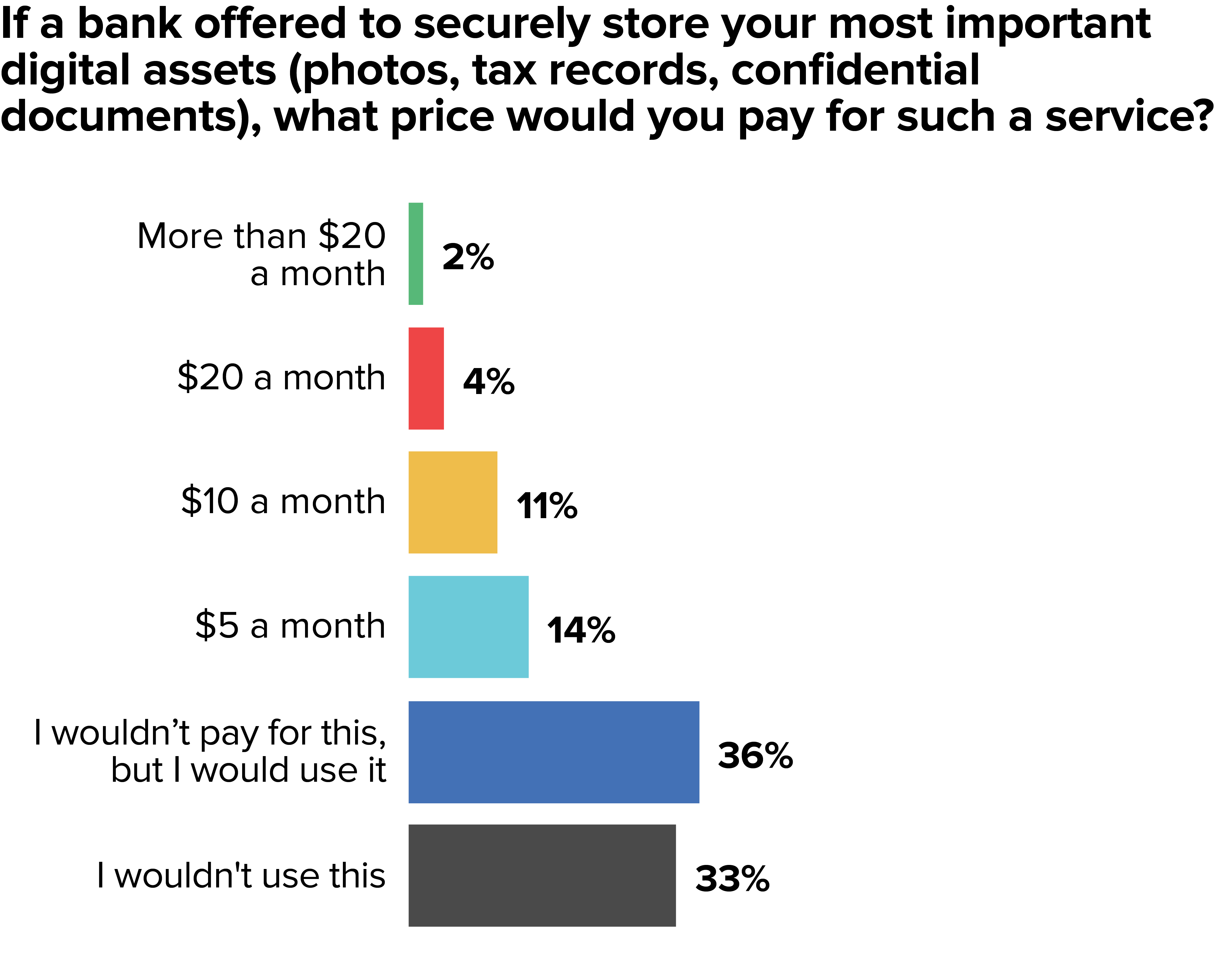

Similar to expressing an interest in smarter identity and credit protection, people want a safe way to store their most valuable digital assets. Chris Skinner, author of Digital Bank, says that a major value proposition of banks will be securely storing people’s most important digital assets.

When we asked people about this service, 31% said they’d pay at least $5 a month for it and nearly 40% said that though they wouldn’t pay for the service, they would use it. This signifies that this service has the potential to become a differentiator for the bank of the future.

MX Research, Survey of 1,000+ US consumers

MX Research, Survey of 1,000+ US consumersTo do offer data protection for digital assets, financial institutions might partner with fintech companies such as EverSafe, CertainSafe, and Johnson Controls, which specialize on this front. They can also expand internal data solutions by applying the same safeguards for financial data and allow customers to upload digital assets such as photos, tax records, and confidential documents.

Just as new cars include lane sensors, vehicle avoidance indicators, and cameras to give warnings so people can avoid accidents, financial institutions should likewise automatically guide customers toward financial health and away from financial disasters.

There have always been people who, despite their best efforts, don’t keep a budget. Even those who do keep a budget struggle to do it actively. It’s either too much work, or their expenses and income change so dramatically month to month that it’s impossible to permanently lay down consistent restraints. It all leads to financial anxiety.

This is where automated financial guidance comes into play. Through the use of advanced algorithms, customers can view their expenses in terms of fixed costs (such as rent, food, and loans), investments (particularly retirement accounts), short-term savings goals (such as vacations), and money that is available to spend. From there, they can get automated insights and nudges on how they can consistently develop financial strength in their day-to-day decisions.

MX gives financial institutions such a product — a newsfeed of personalized insights to empower users to be financially strong. Users can view a list of everything they currently subscribe to (and might be surprised to know how much it all adds up). They can also see notifications about how they’re doing in real time and even see offers for products that might be a better fit for them, a feature that 94% of consumers say they want.

Want to read about the other features listed in the survey? See the Ultimate Guide to the Future of Banking.

March 4, 2026 | 3 min read

Jan 2, 2026 | 3 min read

Dec 3, 2025 | 3 min read